2026 Trends for Drone Service Providers in Utility Inspection

Your best pilot just quit. The replacement is Part 107 certified, a thousand hours logged, perfectly capable. But he captures insulators at a slightly different angle. He doesn’t frame conductor hardware the way the first guy did. He doesn’t know that this particular utility needs close-ups of every vibration damper because their asset team uses those images to model fatigue life.

Three weeks later, the utility rejects 30% of the deliverable. You eat a reflight.

If you run a drone service provider serving electric utilities, some version of that story has happened to you. And here’s the harder truth: the market dynamics of 2026 are about to make it happen more often, to more operators, at higher stakes.

- Utilities are pulling inspection work in-house.

- Autonomous docking systems are automating the routine jobs.

- BVLOS is about to flood your pipeline with ten times the data volume.

- The DJI ban is forcing fleet transitions mid-contract.

- And AI analytics are redefining what “valuable data” even means.

Some of those shifts are opportunities. Others could put you out of business. Here’s what’s what’s actually happening, what it means for your operation, and where the sharpest DSPs are placing their bets.

Top Utility Industry Trends at a Glance

Will Utilities Replace Drone Contractors with In-House Programs?

Nobody at drone industry conferences wants to ask this out loud, so here’s the direct answer: partially, yes.

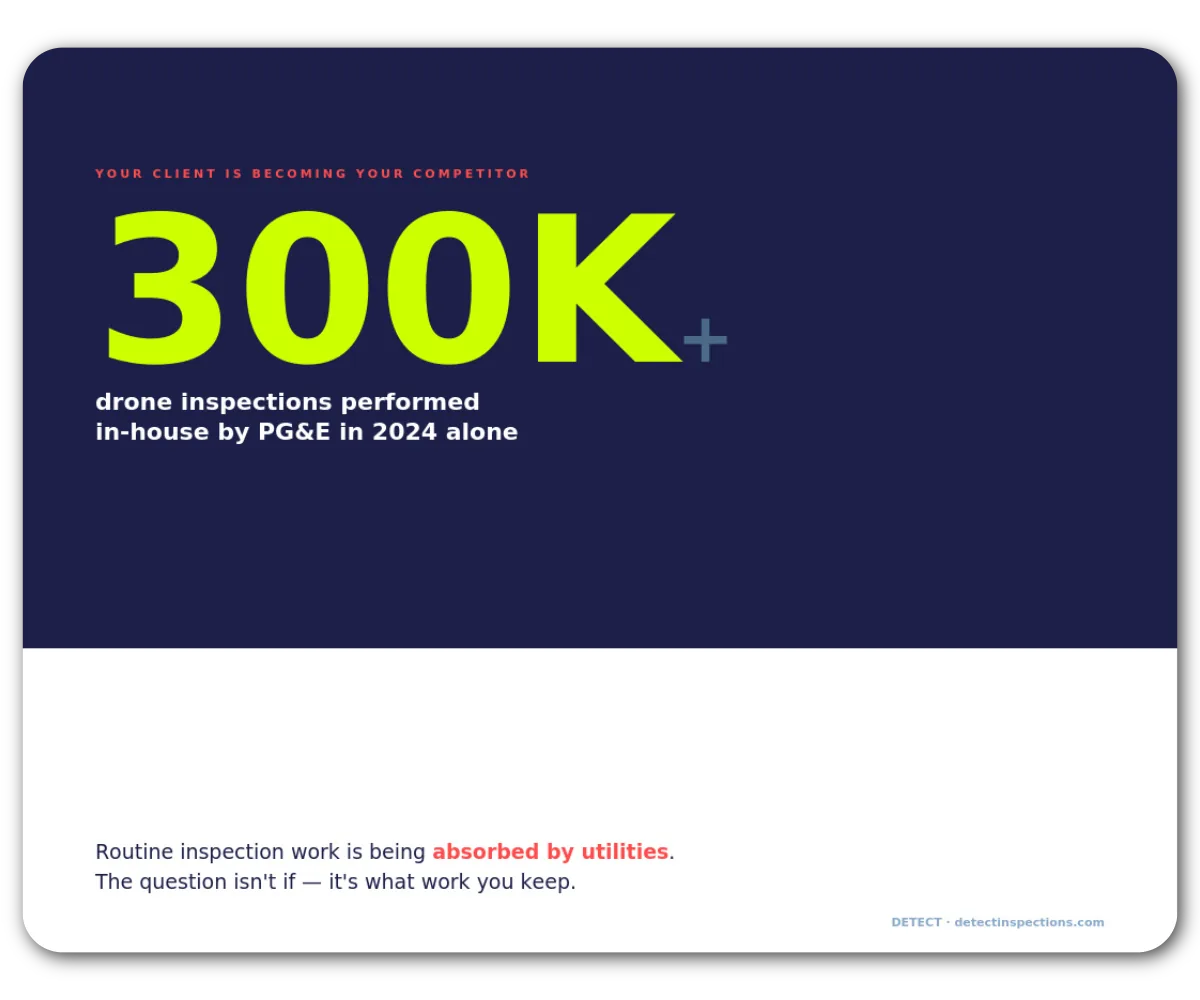

- PG&E logged over 300,000 drone inspections in 2024 and has been steadily moving portions of its program from contractors to internal teams.

- ComEd expanded its fleet with Skydio X10 platforms.

- Southern Company, AEP, Dominion, and NYPA are all building or scaling internal capabilities.

The economics aren’t subtle: an in-house program costs $25,000–$50,000 to launch with $10,000–$20,000 in annual operating costs. For a utility running hundreds of inspections per year, the math beats per-mile contractor pricing fast. Internal teams also build institutional knowledge about specific assets that rotating contract crews never pick up.

The full story is messier, though. Most utilities are landing on a hybrid model: internal teams handle routine, high-frequency inspections while external DSPs take on specialized missions, surge capacity, BVLOS corridor work, and advanced sensor payloads. PG&E itself still relies heavily on contractors for the complex stuff.

DSPs aren’t going away. But routine inspection work is commoditizing, and the DSPs who survive the in-house shift are the ones offering capabilities the utility can’t replicate internally: analytics-ready data, multi-sensor workflows, BVLOS-scale corridor coverage, and — critically — quality infrastructure that guarantees consistent deliverables regardless of which pilot is flying.

If the utility’s internal team can do what you do with a cheaper Skydio and a lineman who took a two-day course, you’re not a partner. You’re a line item waiting to be cut.

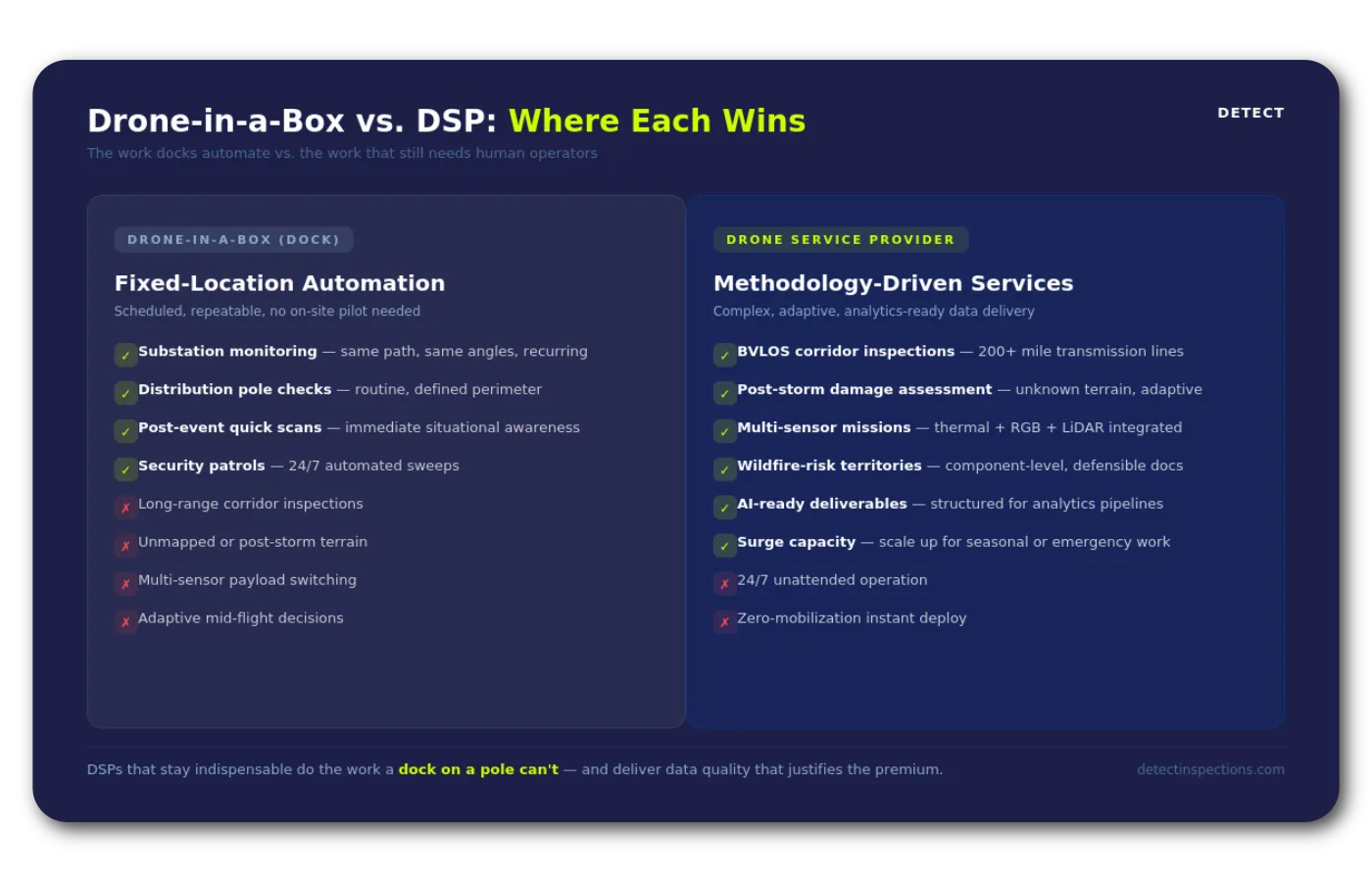

Can Drone-in-a-Box Systems Replace Drone Service Providers?

In-house programs squeeze DSPs slowly. Autonomous docking systems move faster. Skydio Dock lets utilities fly scheduled, repeatable inspections from a weatherproof station — no on-site pilot. The marketing copy says it plainly: drones that launch, fly, land, and recharge without human intervention. Southern Company is an early-access partner, using docks for post-event substation inspections. Percepto, Censys+STRIXDRONES, and others are offering similar persistent-intelligence platforms.

For substation monitoring and routine distribution checks, these systems are becoming viable. They fly the same path every time. They capture consistent data. They feed it directly into analytics platforms. That’s a real slice of the DSP market disappearing into automation.

But docks are fixed-location:

- They don’t cover 200-mile transmission corridors.

- They don’t do post-storm damage assessments in terrain nobody’s mapped.

- They can’t adapt mid-flight when a structure configuration doesn’t match the asset database.

The work that requires judgment and multi-sensor complexity still needs a human behind the sticks. The DSPs that stay essential are the ones flying missions a dock on a pole can’t, and delivering data quality that justifies the premium over what an autonomous system produces on autopilot.

How Will BVLOS and FAA Part 108 Change Drone Inspection Contracts?

BVLOS tilts the field back toward DSPs — if they position for it:

- The FAA’s Part 108 NPRM, published August 2025, proposes a standardized approval pathway that replaces the per-mission waiver purgatory operators have endured for years.

- An executive order signed the same summer accelerated the timeline.

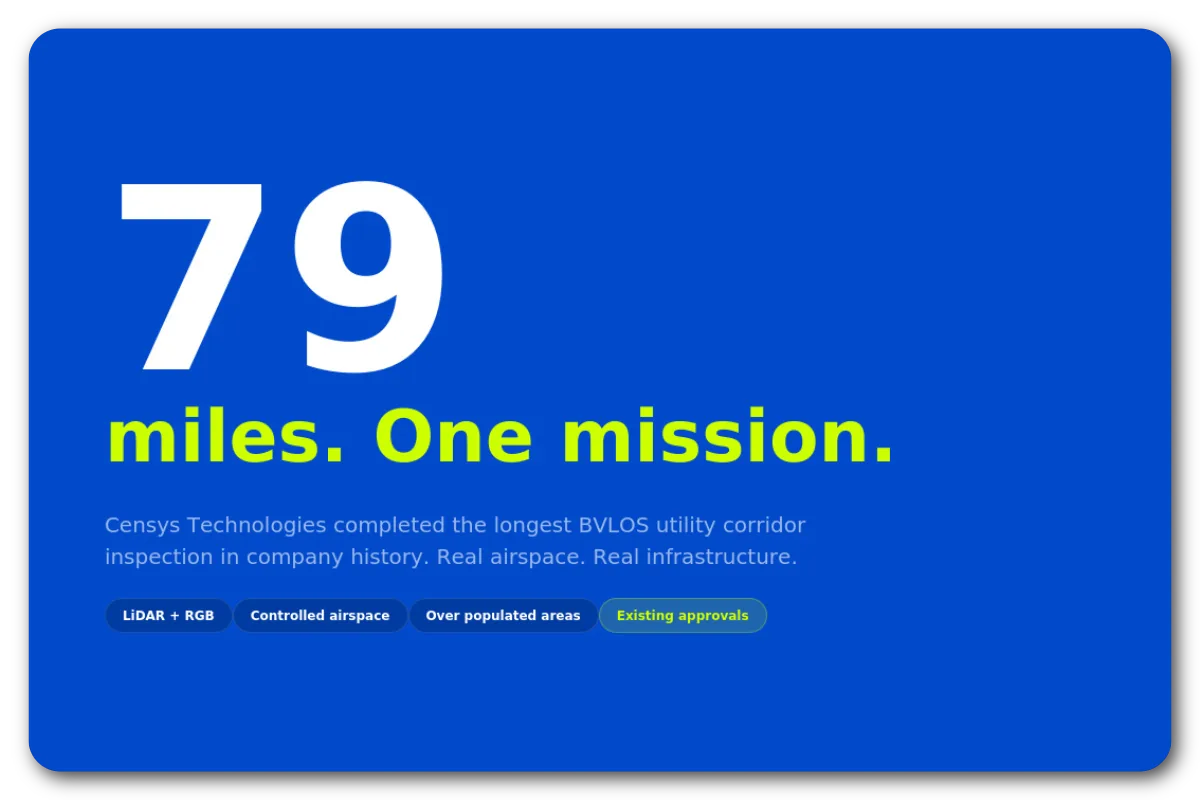

- In February 2026, Censys Technologies demonstrated what this looks like in practice: a 79-mile BVLOS mission over Florida utility corridors.

Utilities won’t do this work in-house, and docks can’t do it from a perch. Multi-hundred-mile corridor inspections require BVLOS-capable aircraft, specialized crews, regulatory expertise, and — here’s the part that gets overlooked — a data pipeline that can handle the volume. UAV News has estimated a tenfold increase in captured imagery once BVLOS becomes routine. Everyone repeats that stat. Few have worked through what it means operationally.

Here’s what it means: if your current QA process involves a human reviewing images on a laptop, and it takes your team four hours to validate a 200-structure inspection, BVLOS-scale corridors will produce workloads you cannot clear in a day. Not because your people are slow. Because manual review doesn’t scale linearly. Fatigue sets in by hour three. Missed components compound. Your best reviewer starts making the same errors your newest pilot makes.

The DSPs winning BVLOS contracts won’t have the longest-range aircraft. They’ll have quality infrastructure that scales without depending on any single person.

What Does the DJI Ban Mean for Utility Drone Operators?

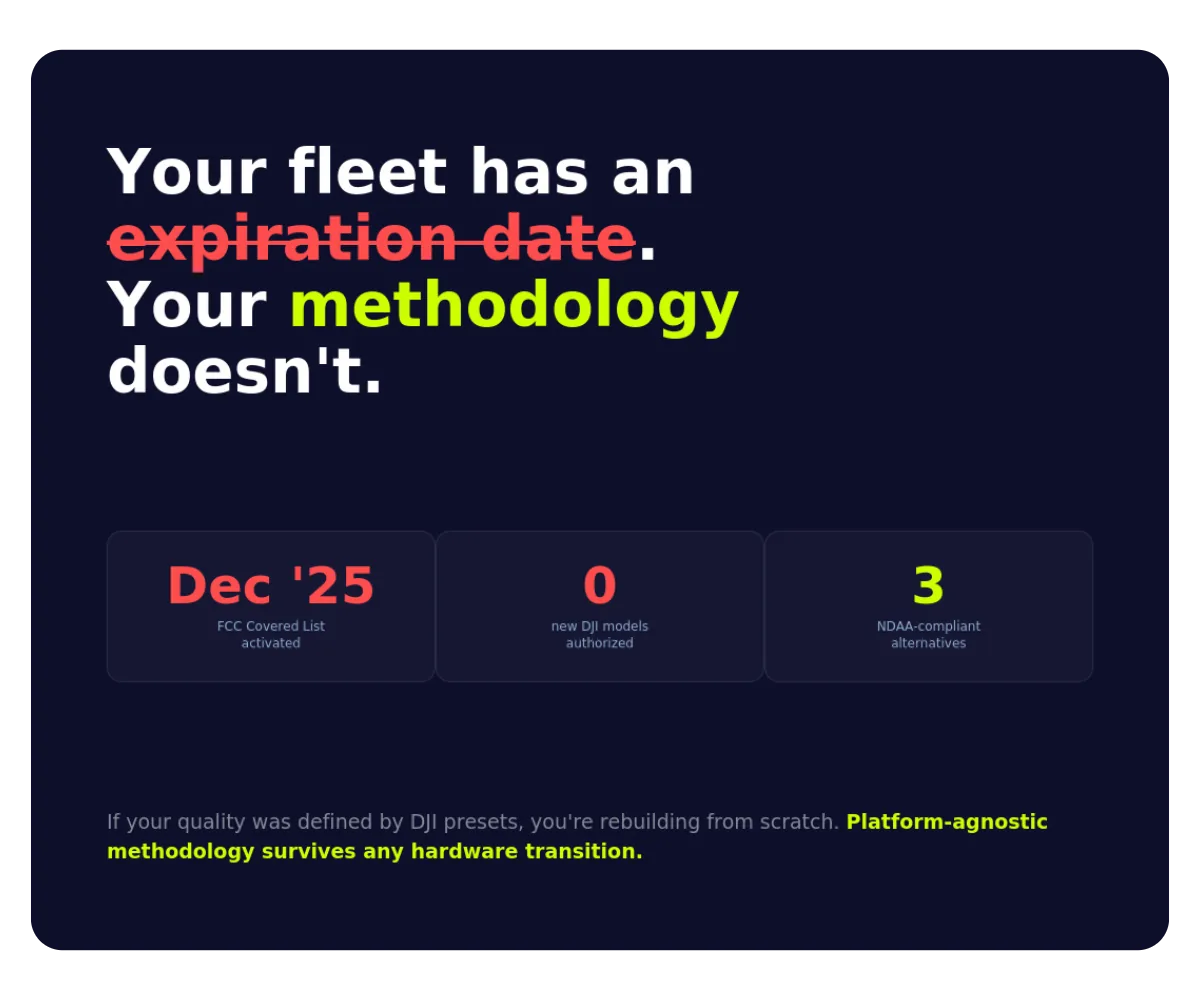

Most DSPs built their operations on DJI hardware. The Matrice 300 and 350 RTK became the default utility inspection platforms because they were capable, affordable, and well-supported. Flight plans were built around their sensor payloads. Pilots trained on their controls. Spare parts were a phone call away.

Then, in December 2025, the FCC added all new foreign-made drones to its Covered List. The 2025 NDAA had given a security agency one year to clear DJI. Nobody did. The automatic consequence activated. Existing hardware flies legally, but new equipment, parts, and firmware support are constrained and tightening. Utilities with government contracts increasingly mandate NDAA-compliant platforms — Skydio X10, Freefly Astro, Inspired Flight. That mandate isn’t going to soften.

For DSPs, this procurement crisis compounds monthly. But the real problem gets buried under the hardware noise: if your quality was defined by your DJI preset configurations and your senior pilot’s muscle memory, you’re rebuilding from scratch.

If your capture standard lives in a documented, platform-agnostic methodology — resolution thresholds, angle requirements per component, metadata specs — the hardware transition is disruptive but survivable. The methodology doesn’t change. The platform does.

Why Utility-Grade Data Quality Is the New Competitive Advantage

Every trend in this article leads to the same place. In-house vs. contractor, BVLOS corridor, dock-based autonomy — the utility’s question is always the same: does the data meet the standard our analytics pipeline requires?

According to the National Grid Partners survey, 42% of utilities plan targeted AI deployments within two years. AI-powered defect detection and predictive maintenance require structured input: correct asset association, consistent resolution, complete component coverage, reliable metadata. A sharp image of the wrong component doesn’t just waste time — it poisons the analytics pipeline.

We see this at Detect constantly. A DSP delivers 8,000 images from a corridor inspection. Technically sharp. Flight was efficient. The pilot did a professional job by any reasonable visual standard. But 15% of the images are mis-associated due to uncorrected GPS drift because GPS drift went uncorrected. Another 10% are missing component coverage — no close-up of the vibration dampers because the pilot had never been told that this particular utility uses those images to model fatigue life. The DSP thinks they delivered a successful project. The utility sees a 25% quality gap. Nobody is lying. They’re measuring different things.

The gap between what DSPs think they’re delivering and what utilities actually receive is the most expensive problem in this industry that nobody has put a number on.

The consequences reach past rework costs. In wildfire-prone corridors, every captured image is potential evidence:

- The Camp Fire investigation attributed a catastrophic failure to inadequate inspection.

- PG&E found 95% of wildfire risk concentrated in just 22% of their lines. In those corridors, the documentation standard isn’t “good enough.” It’s “defensible in a courtroom.”

Even brand-new infrastructure carries risk: in one case, DetectOS caught a loose clevis bolt on a newly energized HVDC line that could have caused a million-dollar outage.

Grid security adds another layer: NERC’s GridEx VIII exercise found utilities can’t yet distinguish authorized inspection flights from hostile drone approaches. DSPs without documented, pre-approved flight plans and auditable data chains aren’t just vendors. They’re security variables.

How DSPs Can Win and Retain Utility Contracts in 2026

The market is splitting in two. One side: routine work pulled in-house or handed to docking systems. The other: high-value inspection services built on methodology that utilities can’t replicate and docks can’t perform. Every section of this article points at the same fault line.

The DSPs landing utility contracts right now have a few things in common:

- Their capture methodology is documented and platform-agnostic — it works whether the crew is flying a Skydio X10 or a legacy DJI Matrice.

- Their QA scales with data volume, not headcount. Their deliverables feed directly into AI analytics without manual remediation.

- Their flight procedures satisfy both procurement and security requirements.

- And they’re pursuing the advanced work — BVLOS corridors, multi-sensor missions, wildfire-risk territories — that neither autonomous systems nor utility linemen with two days of drone training can handle.

The DSPs bleeding work share patterns too: pilot-dependent quality that varies crew to crew, manual QA that breaks at scale, hardware-locked workflows disrupted by the DJI ban, and raw imagery deliverables that force the utility to do the hard work of structuring the data before their analytics can touch it.

What it comes down to: the DSP delivering utility-grade data from day one stops competing on price. They compete on trust. In 2026, trust runs on methodology — not hardware, not headcount, not the lowest per-mile bid.

Detect’s Data Quality Program exists because we kept seeing the same problems from the analytics side — inconsistent capture, mis-associated images, component gaps — and decided to automate quality validation at the source. The DQP standardizes capture methodology across platforms, automates quality validation while crews are still on-site, and trains pilots on the component-level awareness that turns good flying into utility-grade data. It’s not the only path forward. But if any of this hits close to home, it’s worth talking.

Start your Detect partner program now!

Frequently Asked Questions

How much does it cost for a utility to build an in-house drone inspection program?

Expect to spend $25,000 to $50,000 on equipment, pilot training, and software licensing upfront, then $10,000–$20,000 per year to keep it running. At scale — hundreds of inspections annually — the math usually beats contractor pricing. That said, most utilities still run a hybrid setup: in-house teams handle the routine stuff while DSPs cover BVLOS corridors, multi-sensor missions, and surge capacity.

What NDAA-compliant drones can replace DJI for utility inspection?

The main contenders on the Blue UAS and Green UAS Cleared Lists: Skydio X10 (AI-powered autonomy, 360-degree obstacle avoidance), Freefly Astro Prime (modular, open-ecosystem mapping), and Inspired Flight IF800 Tomcat (heavy-lift, customizable payloads). They each trade off differently on flight time, sensor integration, and pilot learning curve versus the DJI Matrice series. What matters most is building a platform-agnostic capture methodology so your deliverable quality holds up through the switch.

How will BVLOS and FAA Part 108 affect drone inspection contract pricing?

BVLOS lets DSPs cover full transmission corridors in single missions, no relay pilots needed, which crushes unit economics in the right direction. The catch: missions generate up to ten times more imagery, and that volume breaks manual QA. DSPs investing in automated quality validation will keep the margin gains. Everyone else will watch rework costs swallow the efficiency.

Can drone-in-a-box systems fully replace drone service providers?

Not yet, and probably not fully. Docking systems like Skydio Dock are built for fixed-location, scheduled inspections — substations, distribution equipment, and defined perimeters. They fall apart on long-range BVLOS corridor work, post-storm damage assessment in unmapped terrain, and adaptive multi-sensor missions where a pilot has to make real-time calls. DSPs doing that higher-complexity work aren’t going anywhere.

What percentage of drone inspection images get rejected by utilities?

Numbers vary across the industry, but Detect’s own analysis consistently puts the figure at 15–25% of delivered imagery needing remediation before AI analytics can touch it — — GPS-based mis-association, missing component coverage, resolution inconsistencies. On fixed-fee contracts, the DSP eats that rework cost. Standardized capture methodology and automated field QA are the two fastest ways to close that gap.

What do utilities actually look for when evaluating drone inspection vendors?

Price per mile is table stakes. After that, utilities look at data quality track records, turnaround commitments, scalability across large asset portfolios, NDAA compliance, safety documentation (ISNetworld prequalification), and whether deliverables plug directly into analytics and GIS/CMMS systems without manual cleanup. More and more, the ability to deliver AI-ready, structured data is what separates a strategic partner from a commodity vendor.